Sustainable aviation fuel: eSAF found to be 13 times the cost of regular aircaft fuel

Argus, an energy and commodity market intelligence firm, has launched the aviation industry’s first calculated price indexes for electrolytic sustainable aviation fuel (eSAF). It shows the current cost of eSAF is thirteen times that of fossil-based jet fuel.

The firm aims to address the urgent need of aviation fuel suppliers, airlines, and policymakers for clear pricing as they work toward meeting industry mandates.

In a brief on the new price index, Argus notes that while Europe and the UK are advancing toward more stringent SAF requirements, there is a widening disconnect between policy ambition, cost realities and investment delays.

Read more: EU’s €2bn SAF subsidy doesn’t fix the real issues

Argus eSAF indexes show the scale of the challenge

Argus’ newly launched weekly indexes calculate the production cost of eSAF in the Amsterdam–Rotterdam–Antwerp (ARA) region, in both €/t and $/t, and are published both including and excluding capital expenditure.

The November 2025 cost assessment shows eSAF is currently:

- 13× the cost of fossil jet fuel

- 3.5× the cost of HEFA-SPK bio-SAF

This structural price gap will persist, Argus argues, as long as hydrocarbon jet fuel prices fail to reflect their environmental cost. Governments will need to provide long-term policy support to bridge it.

SAF is the only near-term path to reducing aviation emissions

Since electric propulsion or hydrogen aircraft will require a decade or more of engine redesign and infrastructure overhaul, SAF remains the only saleable option today capable of reducing aviation emissions without modifying existing aircraft or airport systems.

Europe and the UK began their SAF mandates this year with an initial 2% requirement, ramping sharply through 2035 as part of their net-zero roadmap.

European Union – ReFuelEU Aviation

- Starting at 2% SAF of the total jet-fuel supply in 2025.

- Rising to 6% by 2030.

- Then to 20% by 2035.

- Long-term target: 70% by 2050.

- There is also a sub-mandate for synthetic (PtL/eSAF) fuels: starting at 0.7% in 2030 and increasing to 35% by 2050.

United Kingdom – SAF Mandate

- Mandatory SAF share begins in 2025 at 2% of total UK jet-fuel demand.

- Increases to 10% by 2030.

- Reaches 22% by 2040.

- Additional UK sub-target for PtL SAF starting at 0.2% by 2028 and reaching up to 3.5% by 2040.

Read more: Which European airlines use the most SAF?

Airlines are not optimistic about finding an adequate, affordable SAF supply

Under pressure, the airline industry is questioning the viability of SAF mandates.

Ryanair CEO Michael O’Leary has been openly sceptical. As reported by the BBC this August, he said there is “not a hope in hell” of the UK’s 10% SAF mandate being met by 2030. O’Leary also said that Ryanair would not increase its SAF use because supply “is not there,” and described SAF as “nonsense.”

IATA argues that governments must support the development of technology that would stabilise SAF supply and make it more affordable. Ahead of this year’s ICAO Assembly, IATA Director General Willie Walsh said SAF was “absolutely critical” for airlines to meet their net zero targets by 2050.

“We’re disappointed at the progress made in relation to production. It’s not where we need it to be,” he said. “The problem, as we see it, is one of supply and not one of demand.”

Policymakers, however, are holding to their targets, requiring aviation to decarbonise alongside other transport modes, while failing to address the production gap.

Argus sees SAF oversupply today, and a crisis by 2030

Argus forecasts a global oversupply of SAF until around 2030, when EU mandates become far more stringent and penalties begin to bite.

Conventional jet fuel suppliers face billions of dollars in potential fines if they fail to meet SAF quotas. At the same time, airlines must refuel with SAF-blended jet fuel at major EU airports or absorb penalties for tankering fuel from elsewhere.

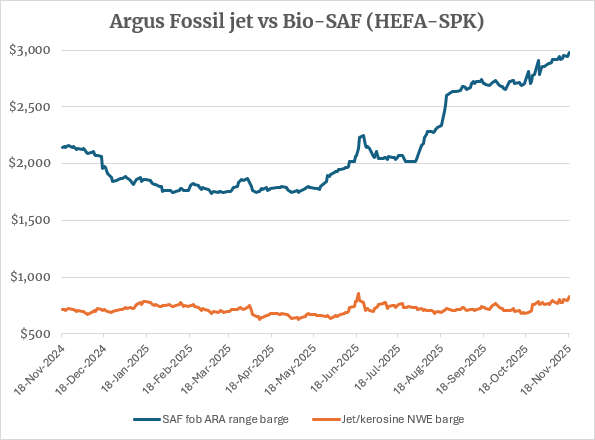

Current SAF pricing discourages greater adoption. In northwest Europe, SAF prices recently surged to a two-year high—nearly $3,000 per tonne, more than 3.5 times the cost of conventional jet fuel—despite the overall oversupply.

Argus attributes this temporary tightening to factors such as plant maintenance and weak imports. Yet even as prices rise, major producers, including BP and Shell, have delayed or cancelled SAF projects, citing economic and policy uncertainty.

Argus says there is growing awareness that bio-SAF alone cannot decarbonise aviation. Feedstocks such as used cooking oil—on which HEFA production depends—are finite and structurally insufficient for the scale of demand.

eSAF mandates loom, but industry is unprepared

Hydrogen-derived eSAF will become mandatory in the EU from 2030, but Argus believes the supply chain is nowhere near ready to deliver.

To meet quotas, the region will require roughly 600,000 tonnes of eSAF annually, equivalent to about 12 commercial-scale plants. Yet of the 70 proposed UK and EU eSAF projects tracked by Argus, not a single one has reached a final investment decision (FID).

Plant construction takes three to four years, meaning FIDs must be taken within the next year for Europe to have any chance of meeting 2030 obligations. The risk of non-compliance will have serious financial consequences.

If no eSAF is available in 2030, penalties for EU fuel suppliers could total $5–10 billion, and obligations roll forward annually. According to Argus, the ongoing debate over whether the EU would enforce such penalties has further dampened investor confidence.

A SAF Catch-22 is blocking investment

Argus believes a fundamental misalignment between supply and demand hampers the financing of eSAF projects. Long-term offtake agreements are necessary to secure funding for these projects.

However, airlines, which typically operate with tight margins and favour short-term fuel contracts, are hesitant to commit tens of millions of dollars upfront for a fuel whose price might decrease as the technology evolves. This conflict is the primary factor stalling investment across the e-SAF sector.

“Long-term eSAF offtake agreements are essential to the financing of production facilities,” said Argus Media chairman and chief executive Adrian Binks. “But buyers are wary of committing tens of millions of dollars to such agreements, creating a disconnect between supply obligations and demand that has stalled investment.

“Our new modelled costs will provide important independent transparency upon which participants across the e-SAF value chain can rely to inform their long-term decision making.”

The new eSAF indexes add to Argus’ established SAF benchmarks in Northwest Europe, Asia-Pacific and the US, leveraging the organisation’s pricing and consultancy depth across biofuels, natural gas and hydrogen.

With mandates accelerating, penalties looming and investment lagging, the industry faces a narrowing window to align supply capacity with regulatory expectations. Argus expects its data will give airlines, refiners, and policymakers a clearer view of the fundamental economics of eSAF—precisely when informed decision-making is most urgent.

Get all the latest commercial aviation news on AGN here.

Featured Image: World Energy