SkyNRG SAF outlook warns market is scaling but post-2030 supply gap remains

The sustainable aviation fuel market is growing, but not quite in the way earlier forecasts expected.

SkyNRG and ICF’s 2026 SAF Market Outlook, launched during the Sustainable Aviation Futures Congress in Amsterdam, suggests SAF has moved from early voluntary uptake into a more mature, mandate-led market.

But the report also points to a more cautious outlook for 2030, with weaker US demand, continued reliance on HEFA and slow progress on advanced pathways all raising questions about whether aviation will have the right supply available when demand accelerates.

SkyNRG cuts 2030 SAF demand forecast

Global SAF supply is estimated to have doubled again in 2025 to around 2 million tonnes, up from 1 million tonnes in 2024. Demand is expected to rise to around 3 million tonnes in 2026, equal to roughly 0.9% of global jet fuel demand.

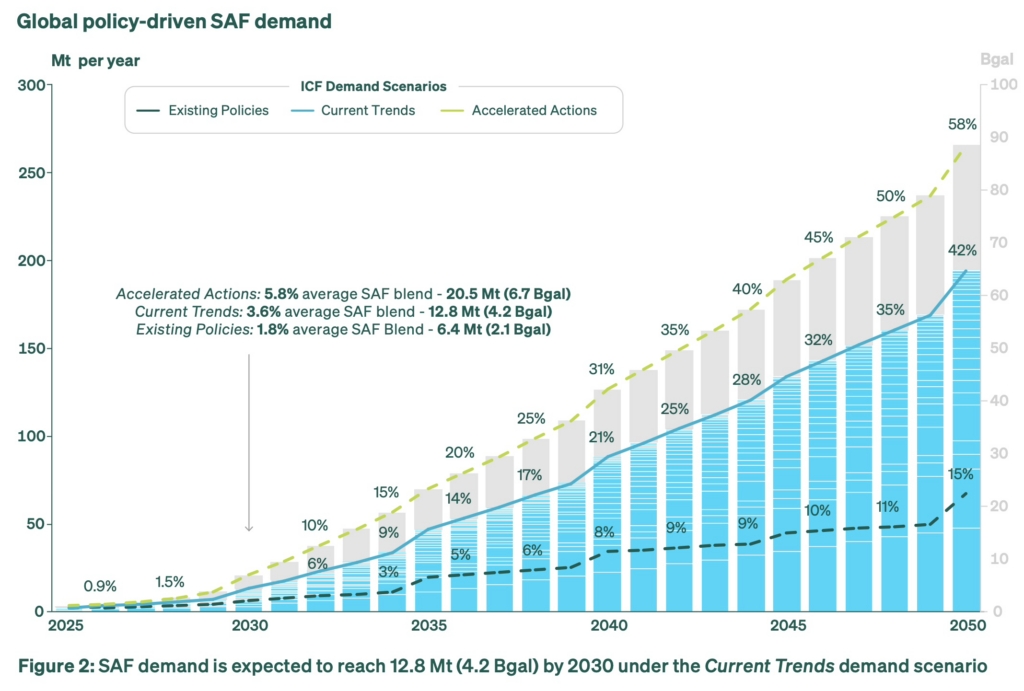

By 2030, SkyNRG and ICF expect global SAF demand to reach 12.8 million tonnes under their Current Trends scenario. That would represent around 3.6% of global jet fuel demand.

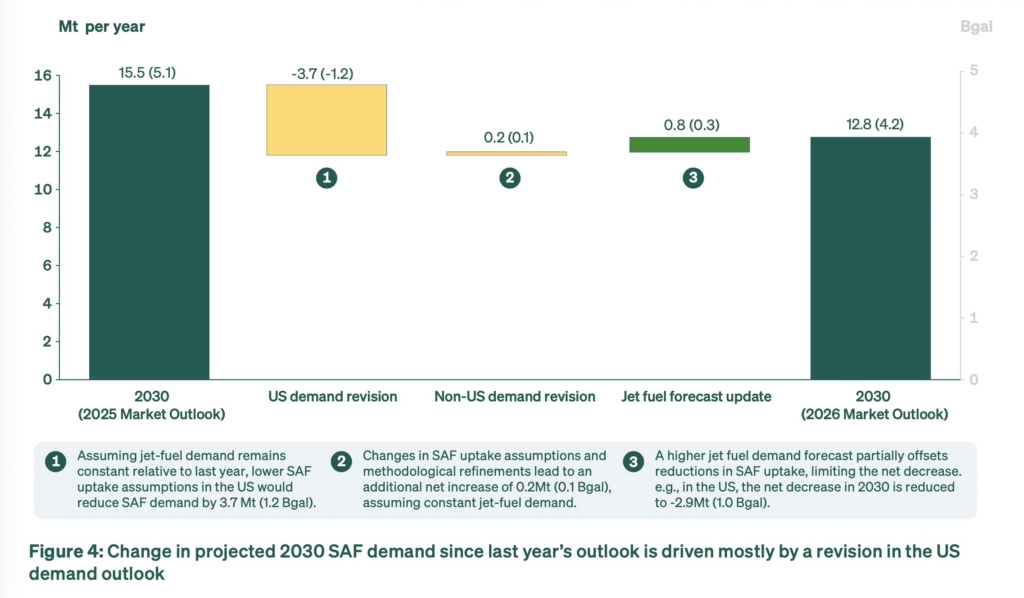

However, that figure is a significant downgrade from last year’s outlook, which forecast 15.5 million tonnes of SAF demand by 2030.

SkyNRG said the revision is mainly driven by weaker near-term demand expectations in the United States, where recent policy changes have reduced the relative attractiveness of SAF compared with renewable diesel. The report said changes to US incentives have weakened the near-term business case for SAF, while stronger support for road-fuel biofuels continues to pull feedstock and producer interest towards renewable diesel.

The downgrade has been partly offset by stronger policy momentum elsewhere. SkyNRG highlighted Europe’s binding SAF mandates, alongside policy development in countries including Indonesia, South Korea, Singapore, Japan, Australia and Brazil.

SAF capacity looks sufficient, but only on paper

The supply picture initially appears more reassuring.

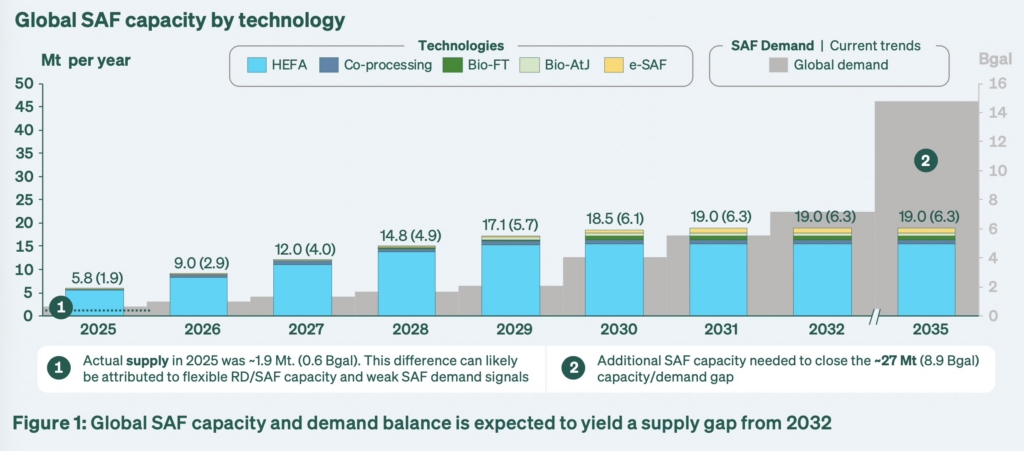

SkyNRG and ICF expect global SAF production capacity to reach 18.5 million tonnes by 2030, slightly higher than the 18.1 million tonnes projected in last year’s outlook.

On paper, that means announced capacity is more than enough to meet the report’s 12.8 million tonne demand forecast for 2030. But SkyNRG cautions that this apparent comfort could be misleading.

The report warns that the market may enter a period of temporary overcapacity before 2030, followed by a much tighter supply position once demand starts to accelerate in the early 2030s. Weak demand signals could put pressure on producer margins, reduce utilisation rates and delay final investment decisions.

SkyNRG said around a third of tracked SAF projects have been delayed by at least one year compared with last year’s outlook. Delays were seen across all major pathways, but were more pronounced in advanced routes beyond HEFA.

By 2035, global SAF demand is expected to reach around 47 million tonnes. Current projected capacity reaches only around 19 million tonnes by then, leaving a sizeable gap unless additional projects move through financing, construction and commercial operation.

That makes the next few years critical. The issue is no longer simply whether SAF projects are being announced, but whether they can be turned into operational plants quickly enough.

HEFA remains aviation’s SAF bottleneck

The report also reinforces one of the most persistent tensions in the SAF market: the industry is scaling fastest through the pathway with the clearest long-term constraints.

HEFA, or Hydroprocessed Esters and Fatty Acids, remains the dominant SAF pathway and accounts for around 85% of expected 2030 production capacity. HEFA has been essential in bringing the first meaningful volumes of SAF to market because it is commercially mature and can use existing refining expertise.

But it also depends heavily on waste oils, animal fats and other lipid feedstocks that are already in demand from renewable diesel and other biofuel markets.

SkyNRG said its modelled “HEFA tipping point” remains broadly unchanged around 2030, even though the overall 2030 SAF demand forecast has been revised down. The reason is that the aviation sector’s accessible share of available feedstocks has also weakened, largely because road transport continues to compete for waste oils and lipid-based feedstocks.

In other words, lower demand has not solved the feedstock problem. It has merely reduced one side of the equation while other pressures remain.

The report warned that without diversification beyond HEFA, aviation risks trading one form of energy dependence for another. Europe is particularly exposed, with planned and operational HEFA capacity already exceeding domestic waste oil availability. That could leave the region increasingly dependent on imported feedstocks or imported SAF, even as it leads the world on demand-side regulation.

Advanced SAF pathways are moving too slowly

SkyNRG’s outlook makes clear that post-2030 growth will depend on advanced SAF pathways, including eSAF, Alcohol-to-Jet and Bio-Fischer-Tropsch.

There has been some progress. The report said the global eSAF outlook has strengthened by around 0.8 million tonnes compared with last year, supported by project development in China and stronger policy support in Europe. Global eSAF capacity could reach around 0.6 million tonnes by 2030 and 1 million tonnes by 2031, excluding feasibility-stage projects.

But that remains small compared with the scale of future demand.

Alcohol-to-Jet has moved in the opposite direction. SkyNRG said the expected 2030 capacity from AtJ has been revised down by around 1.3 million tonnes, with project momentum affected by weaker US SAF incentives, competition for ethanol and reliance on a small number of large facilities.

Bio-Fischer-Tropsch has improved slightly, rising to around 0.8 million tonnes of expected capacity by 2030, but the report said commercialisation remains slow.

That concern was echoed during discussions at SAF Congress, where speakers repeatedly pointed to the challenge of moving advanced pathways from technology demonstration and project pipelines into financeable, commercially operating assets. For eSAF in particular, the issue was framed less as a single technology problem and more as a full value-chain challenge involving renewable power, green hydrogen, carbon sourcing, synthesis technology, regulation and offtake.

Europe leads SAF demand as Asia builds capacity

The 2026 outlook also points to a changing global geography for SAF.

Europe remains the clearest demand centre because of ReFuelEU Aviation and the UK SAF mandate. SkyNRG said early evidence suggests first-year obligations were met comfortably in both markets, showing that a functioning compliance market is beginning to emerge.

However, the report also notes practical market formation challenges around pricing transparency, infrastructure, cost pass-through and documentation. Those issues were also raised during SAF Congress sessions, where industry participants said Europe’s first mandate year had created demand but also exposed the complexity of turning regulation into a liquid and efficient fuel market.

Asia, meanwhile, has emerged as the largest source of announced SAF production capacity, overtaking the United States in this year’s outlook. China is described as moving quickly across both HEFA and emerging SAF pathways, supported by industrial policy, faster permitting and coordinated project execution.

Several Asian countries are also seeking to retain more value domestically by moving from feedstock exports towards refining and SAF production. Export controls or restrictions on waste oils and related feedstocks in countries such as China, Indonesia and Malaysia could reshape future SAF trade flows.

For Europe, that creates a strategic tension. The region has the strongest demand signal, but it may still depend on imported feedstocks and fuels unless domestic advanced pathways scale faster.

SAF market moves from optimism to execution

SkyNRG’s 2026 outlook does not suggest the SAF market is failing. On the contrary, it confirms that SAF is becoming a real compliance market, with mandates now creating firm demand in Europe and the UK and policy momentum spreading across other regions.

But it also shows that the next phase will be harder than the first.

The industry is no longer only trying to prove that SAF can be produced and used. It must now prove that the right types of SAF can be scaled, financed and delivered in the right regions before demand rises sharply in the 2030s.

The market is growing. The question now is whether it is growing fast enough, and in the right direction, to avoid a post-2030 supply gap.