Aircraft deliveries hit 7 year high as Airbus and Boeing push toward 2025 targets

December 2, 2025

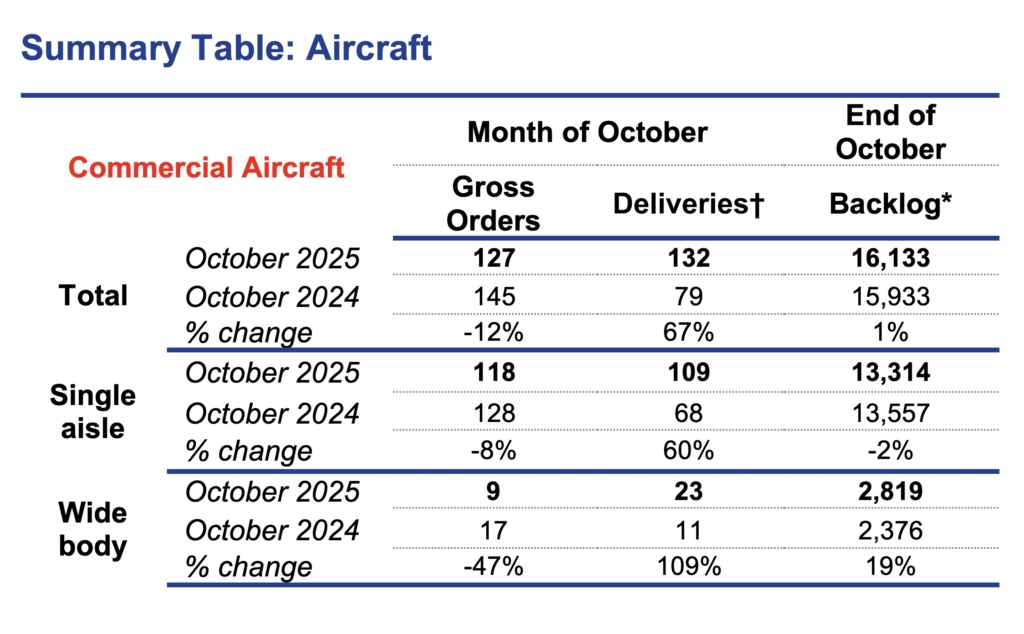

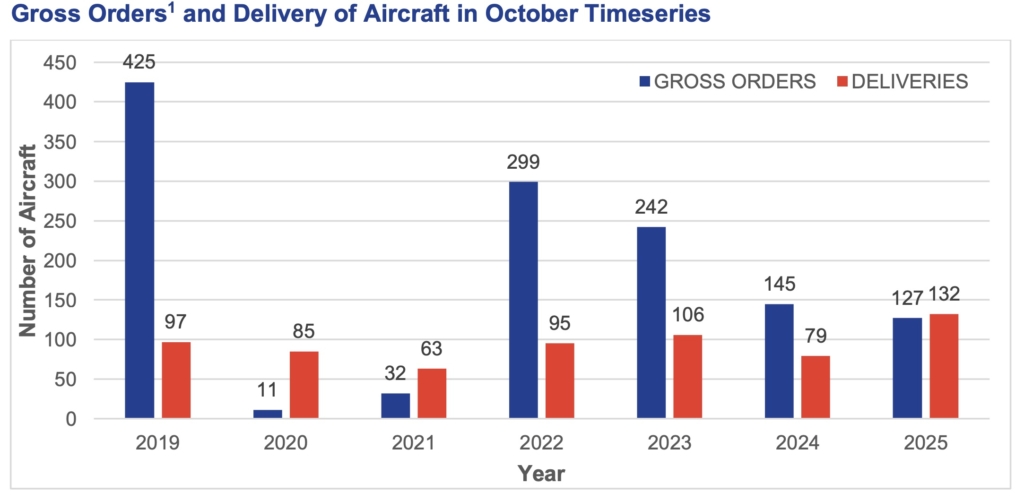

Global aircraft deliveries rose to their highest October level since 2018, with manufacturers handing over 132 aircraft during the month, according to new ADS data.

This represents a 67% increase year on year and the second strongest October ever recorded, narrowly behind the 138 achieved in 2018.

Orders were quieter. ADS recorded 127 aircraft orders in October, down 12% on the same month in 2024 and the lowest October total since 2021. Widebody demand slipped to just nine orders, a 47% decline year on year, with ADS noting that some customers appeared to be holding announcements for the Dubai Airshow.

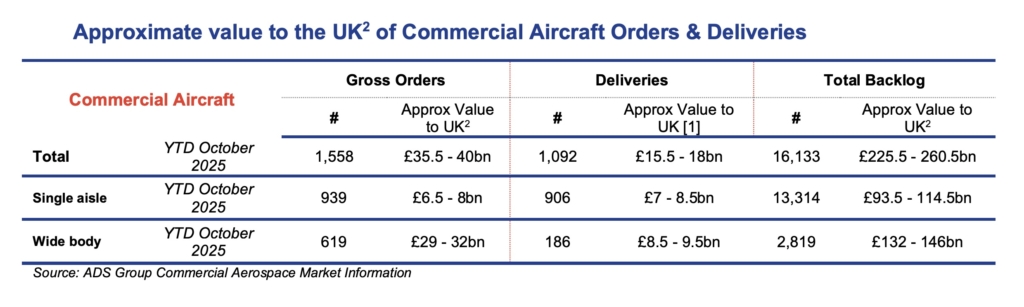

The global backlog remains substantial at 16,133 aircraft. At current production rates, this equates to more than 16 years of work and is valued by ADS at between £225 billion and £260 billion to the UK economy. Narrowbodies make up 13,314 of those aircraft, while the widebody backlog has grown 19% year on year to 2,819 aircraft.

Read more: Did Airbus or Boeing really win the Dubai Airshow?

Airbus and Boeing deliver over 1,000 aircraft as they press towards delivery goals

ADS does not break out OEM totals, but the combined figures indicate that Airbus continued to dominate single aisle deliveries in October, while Boeing contributed a stronger mix of widebodies.

The October spike reflects two clear trends. Widebody deliveries rose 109% year on year, driven primarily by 787, 777F and A350 activity, and single aisle deliveries increased 60% as A320neo and 737 MAX production continued to stabilise.

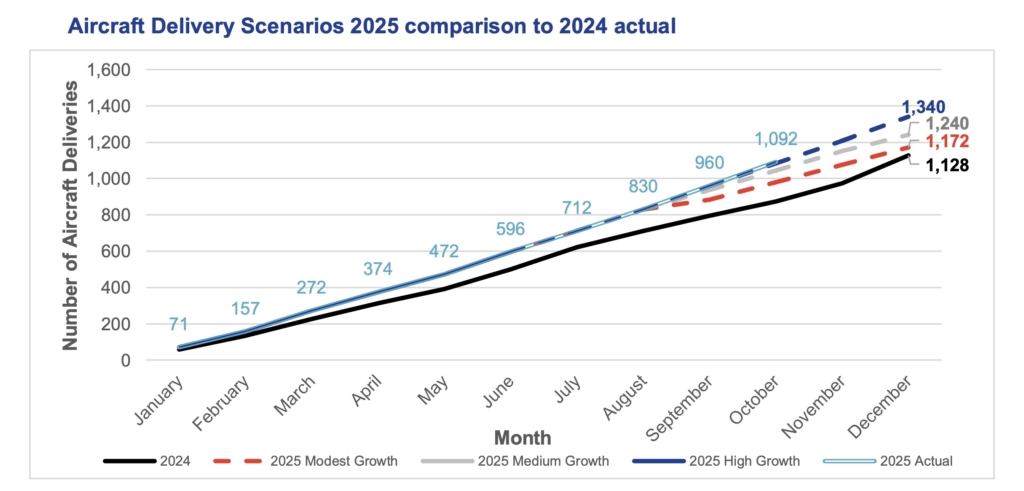

By the end of October, manufacturers had jointly delivered 1,092 aircraft in 2025, which is 25% higher than the same point in 2024. The year-to-date trajectory aligns with ADS’s high growth scenario of 1,340 deliveries by year end, although this relies on the historic pattern of fourth quarter backloading remaining intact.

Airbus continues to work toward phased rate increases on the A320neo family, although engine availability remains a constraint. Boeing has benefited from stable 787 output and continued demand for 777F aircraft, while the 777X programme remained focused on flight test, production readiness and certification milestones across 2025.

Read more: Airbus vs Boeing – Which planemaker is more likely to hit its 2025 delivery target?

Why are so many aircraft being ordered without engine selections?

One notable feature of the ADS dataset is the growing divergence between aircraft orders and engine orders.

In October, ADS recorded 232 engine orders, and not all of these would have been tied to the 127 aircraft orders for the month.

Across 2025, the lack of engine selection has been an ongoing trend as more customers, particularly lessors, are holding out on making powerplant orders.

Several factors are driving this behaviour. Engine supply remains the tightest part of the production system, with both LEAP and GTF deliveries lagging airframe output, and shop visit turnaround times still elevated. Keeping the engine choice open allows customers to select the more reliable or more available option closer to the delivery date.

There is also continuing uncertainty around long-term reliability and maintenance costs. Airlines are seeking clarity on the impact of the PW1100G powder metal inspections and early LEAP durability issues before committing to long-term service programmes that will run for two decades or more.

Lessors are the most active users of this strategy. Many large leasing orders are placed before a future operator is secured, and engine choice has a major influence on lease rates and residual values. Deferring the selection allows lessors to configure each aircraft in line with customer preference and market conditions.

This widening gap between airframe orders and engine selections is likely to persist until engine reliability stabilises and supply chains ease across the single aisle segment.