How geopolitical tension in the Middle East is impacting business aviation

March 14, 2026

With around 700 business jets based in the Middle East, the region has experienced a sharp decline in activity amid rising geopolitical tensions.

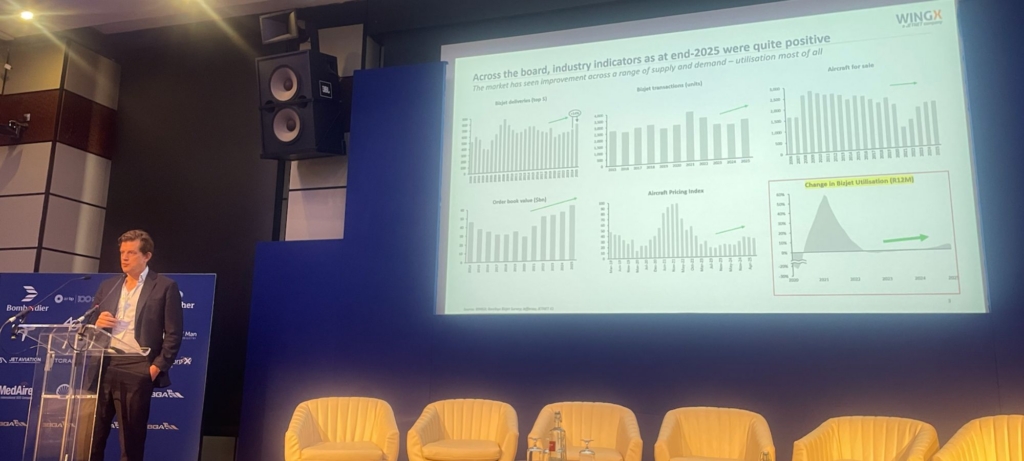

Speaking at the British Business and General Aviation Association (BBGA) AGM on Thursday 12 March, Richard Koe, Managing Director of aviation data specialist WingX, explained that recent data across the UAE, Saudi Arabia, Turkey, and, to some extent, Israel shows that Turkey currently hosts the largest population of business jets in the region.

“In the initial days of the conflict in Iran and across the region, we saw a drop in business aviation activity of around 26%,” said Koe. “At the same time, airline activity fell even further, dropping by around 52%.”

Koe noted that this pattern mirrors what was observed during the COVID pandemic, when aviation activity initially dropped but was then followed by a surge in business jet traffic in 2022.

“It’s perhaps not all that surprising,” explained Koe. “Commercial carriers are often grounded during periods of disruption, whereas business jets continue flying because they provide flexibility and point-to-point connectivity.”

Despite the regional downturn, it has not been a “dramatic decline,” and activity has not stopped completely. Looking at year-to-date figures, Koe revealed that business jet traffic out of Israel is slightly up, while across the Middle East overall it is currently down around 5% compared to the start of the year. He also noted that some activity is still being recorded in Iran, primarily involving smaller jets.

Globally, the Middle East accounts for just 2% of business jet flights, compared with around 5% of commercial scheduled airline operations.

Rise in business charters from the Middle East

WingX’s data also shows that most business aviation flights in the Middle East currently remain within the region. However, Koe said there has also been a recent increase in charter activity from the region to Europe. “Over the past week, we have seen a pick-up in private charters from airports in the Middle East back to Europe, particularly the UK, France and Greece,” he said. “This is likely repatriation traffic, but also aircraft being repositioned away from potential threats.”

WingX has also been monitoring aircraft parked on the ground for customers. “It’s important to consider the representative value of these aircraft,” Koe said. At one point in early March, aircraft worth an estimated US$4.9 billion were parked in parts of the Middle East. In Dubai alone, 51 business jets were recorded on the ground on 3 March, although that number has since dropped to a handful as aircraft have been repositioned.

Impact of rising oil costs

Oil prices are another factor affecting the sector. “We’ve all seen the headlines with fuel pricing rising,” Koe said. “This will inevitably affect the aviation industry and could spill over into the wider economy.”

Fuel accounts for a large portion of operating costs in aviation. For business jets, it accounts for roughly 34% of operating costs, compared with about 25% for commercial airlines. Koe referenced a comment from the CEO of Hong Kong-based Beta Aviation, who revealed that a 30% increase in fuel prices could take out as much as 50% of profit margins.

Looking back over the past two decades, Koe explained that the relationship between oil prices and business jet activity is not always direct. However, there are notable moments where the two align. “In 2008, the last time oil prices were extremely high, we saw a steep decline in business jet activity, but also a recession. So, the two are not entirely unconnected.”

Long-term outlook remains stable

Despite short-term volatility, the long-term outlook for business aviation remains steady. While business jet deliveries have slowed after a surge during the pandemic recovery, this is not uncommon. The market has historically moved in cycles of strong growth followed by periods of consolidation.

“As the industry matures, these swings may become less pronounced,” Koe said, noting that forecasts suggest more stable growth of around 2–3% annually over the coming years.

The global distribution of the business jet fleet has also remained remarkably stable over time. The US continues to dominate the sector. Around 15 years ago, approximately 66% of the global fleet was based in the US. By 2025, that figure had risen slightly to 67%.

The most significant relative growth has been in Asia, where the fleet has doubled in size over the same period, although WingX’s data shows it still represents only around 6% of the global total.

Longevity is another key characteristic of the sector. Of the business jets delivered 50 years ago, around one-third remain in operation today. According to Koe, more than 350 Learjets delivered in the mid-1970s are still flying.

However, Koe cautioned that geopolitical tensions will continue to affect business aviation in 2026 beyond the Middle East. “Growth has plateaued during the first quarter of this year, but we are still seeing around 3% growth in business aviation traffic globally.” He concluded that with business jet deliveries worldwide up 14% and close to pre-covid 2019 figures in 2025, “It is very much a seller’s market.”